| Insurance Requirements Over Lifecycle |

No matter how comprehensive and successful your investment plan may be, the most important asset you and your family have is your health. Without it, you lose your ability to provide for yourself and your family on a day-to-day basis, let alone achieve your long-term goals.

Being injured, or worse, dying prematurely, are subjects we would prefer to keep at the back of our minds. By taking out insurance, you can afford to concentrate on living, knowing that if the worst happens, you and your family will be protected.

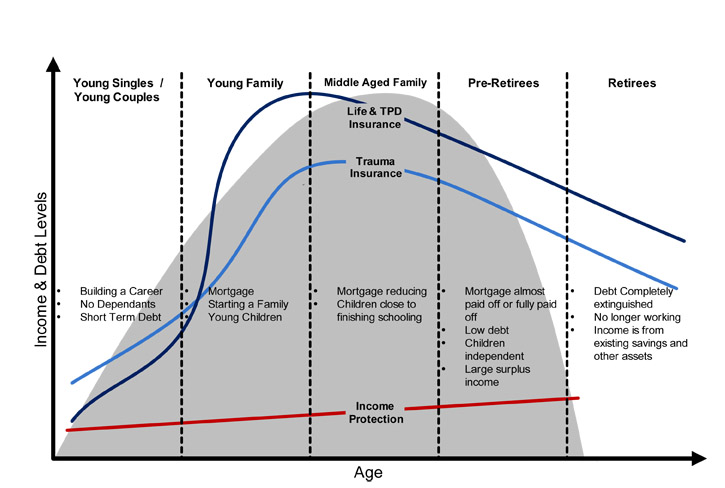

The graph below illustrates how the ideal amount of personal insurance coverage can change over time as you move through different life stages.

| Types of cover |

Life Cover

Also known as ‘term life’ or ‘death cover’, life cover as the name suggests, pays a set amount of money when you die. This money will go to the people you nominate as beneficiaries on your policy.

Total and Permanent Disability Cover (TPD)

TPD pays a lump sum to assist with rehabilitation costs, debt repayments and future living costs if you are totally and permanently disabled. TPD is often bundled with life cover. It is important to note that TPD is usually offered in 2 definitions, ‘own’ or ‘any’. TPD ‘own’ means that you cannot work again in your usual or own occupation. TPD ‘any’ means that you cannot work in any occupation. For this reason, TPD ‘own’ cover is more expensive.

Trauma Cover

Trauma provides cover if you are diagnosed with a specified illness or injury. These policies include the major illnesses or injuries that will make a significant impact on your life, such as cancer or a stroke. It is also referred to as ‘critical illness cover’ or ‘recovery insurance’.

Income Protection

Income protection replaces the income lost through your inability to work due to injury or sickness. There is generally a waiting period of between 15 – 60 days on this insurance, depending on the level of cover and premiums paid. It should also be noted that income protection will cover a maximum of 75% of your gross income for a maximum period of 2 years.

| Some Terms You Should Know |

Income Protection Insurance versus Workers Compensation Insurance

Income Protection is a better cover than Workers Compensation. It provides overall cover, whereas Workers Compensation only covers work accidents and injuries that occur at work. Workers compensation generally does not cover time off work due to illness or accidents that occur outside of the workplace.

Indemnity versus Agreed Value

Income protection policies may be issued as agreed value, guaranteed agreed value or indemnity. An agreed value policy means that the insured monthly benefit, plus any indexation increases, will be payable at the time of claim regardless of any reduction in the insured’s income since commencing the policy. Guaranteed (or financial endorsed) agreed value contracts are those where sufficient financial information has been provided prior to the commencement of the policy to allow a claim for total disablement to be paid without further financial justification. Where this financial endorsement or guarantee does not apply, the financial justification for the insured benefit may be sought at the time of claim.

In all cases, financial information may be sought in the event of a partial disablement claim. In simple terms, providing full financial information at the commencement of a policy makes it less likely that financial evidence will be sought at the time of claim, particularly for claims where the insured is totally disabled and not working.

Indemnity policies provide a limit on the benefit payable, such that at the time of claim, the maximum benefit payable is a factor of the income the insured has earned (generally) in the 12 months leading up to claim. This means that if the insured has suffered a drop in income since taking out the policy, the benefit payable may be less than the insured monthly benefits. Indemnity policies usually cost less than agreed value policies and maybe a discount option on a standard policy.

Standard versus Comprehensive Cover

Standard cover only covers basic features such as the benefit are payable in the event of total disability, partial disability, rehabilitation and unemployment.

Comprehensive cover covers in addition to the basic cover which includes accommodation, family support, home care and specific injuries benefits. Hence, the premium for a comprehensive cover is higher compared to the standard cover.

Cancellable Income Protection Insurance is a policy which may be cancelled and covers you for a short period. The insurance is available from a general insurer. Cancellable income protection insurance may be cancelled at the time of renewal by the insurance company as a result of a health risk, such as a heart attack or development of cancer during the year. This type of insurance is particularly useful to professional sportspersons who may be playing a different sport, or for another club, during the off-season from their usual team.

Non-Cancellable Income Protection Insurance is a policy which guarantees cover to a selected expiry date in return for payment of a premium. Only the insured can void the policy by way of cancellation letter or non-payment of premiums. You must consider Income Protection insurance to assist in covering your financial commitments to ensure that sickness or accident will not create undue hardship or jeopardise your lifestyle.

| Next Step |

As life progresses, your financial circumstances will change. This could be the arrival of a child, the purchase of a property or a new job. When these changes occur, it is important to understand how this may impact your financial situation. Making sure you have sufficient coverage to protect you and your family is imperative for your long-term financial security and peace of mind.

If you are unsure about the levels of cover you require or feel you need to change your level of cover to be adequately protected, please get in contact with us and we will run a full insurance needs analysis for you.

Download this document as a pdf.

Important information and disclaimer

This publication has been prepared by AustAsia Group, including AustAsia Financial Planning Pty Ltd (AFSL 229454).

Any advice in this publication is general only and has not been tailored to your circumstances. Accordingly, reliance should not be placed on the information contained in this document as the basis for making any financial investment, insurance, or other decision. Please seek personal advice before acting on this information.

Information in this publication is accurate as at the date of writing, 20 April 2020. Some of the information has been provided to us by third parties. While it is believed the information is accurate and reliable, the accuracy of that information is not guaranteed in any way.

Opinions constitute our judgement at the time of issue and are subject to change. Neither the Licensee nor any member of AustAsia Group, nor their employees or directors give any warranty of accuracy, nor accept any responsibility, for any errors or omissions in this document.

Any general tax information provided in this publication is intended as a guide only and is based on our general understanding of taxation laws. It is not intended to be a substitute for specialised taxation advice or an assessment of your liabilities, obligations or claim entitlements that arise, or could arise, under taxation law, and we recommend you consult with a registered tax agent.