A Better to Manage Your Mortgage

If you want to repay your mortgage quickly and still have easy access to your additional repayments, an offset account may be worth using.

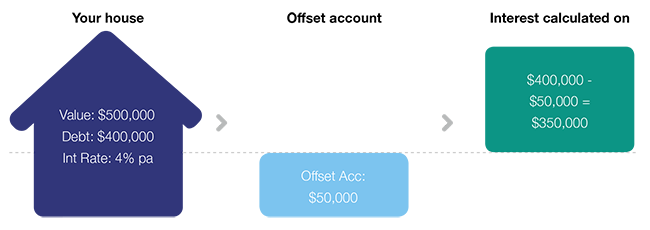

What’s an offset account?

An offset account is a transaction account that is linked to your home loan and the money you deposit in it offsets the loan balance before interest is calculated. For example, if you owe $400,000 on your home loan and have accumulated $50,000 in an offset account, interest will be calculated on $350,000.

Benefits over regular savings accounts

If you hold your surplus cash in an offset account you can save interest at home loan rates, and no tax is payable on the interest savings. This is effectively like ‘earning’ the home loan interest rate tax-free.

Alternatively, you could hold your surplus cash in a regular savings account but the interest rate you earn is usually much lower than what you pay on your home loan. Plus, every dollar in interest you earn is taxable at your marginal rate, which could be up to 47%.1

Benefits over direct loan repayments

When you make additional repayments directly into the loan you can achieve similar benefits to having an offset account. However, limits often apply to the frequency and amount of withdrawals you can make and withdrawal fees are usually charged. With offset accounts, you typically have ready access to the money via an ATM, cheque book and internet, and withdrawal fees are generally not charged.

The best of both worlds

You may even want to have your salary paid directly into an offset account and withdraw money as needed to meet your living expenses. This can enable you to make the interest savings available with direct loan repayments and have easy access to your money.

| What interest rate is earned/saved? | Would interest earned/saved be taxable? | Would you have ready access to the money? | |

| Cash account | Deposit rates | Yes | Yes |

| Direct loan repayments | Home loan rates | No | No |

| Offset account | Home loan rates | No | Yes |

Other things to consider

- If you’d prefer not to have easy access to your additional loan repayments, you may want to make repayments directly into the loan where you are less likely to spend the money impulsively.

- If you would like to credit your salary into an offset account, you should check that your payroll provider is able to do this.

- Some lenders allow you to establish multiple offset accounts to help you better manage your cash flow.

- Some lenders pay an interest rate on the balance of the offset account that is less than the home loan rate. These are known as ‘partial’ offset accounts and are not as effective in saving you interest as an offset account which offsets 100% of the home loan interest rate.

- Offset accounts can usually only be linked to loans with variable interest rates, not fixed rate loans.

- To maximise your interest savings, you may want to pay for the majority of your living expenses on a credit card and repay the card in full before the end of the interest-free period. This enables you to use the credit card provider’s money to fund your living expenses while applying your own funds to reduce your average daily loan balance.

- If you want to invest some of the money held in an offset account, you should consider paying the money directly into your home loan and establishing a separate loan to fund the investments. By taking out a new loan for investment purposes, the interest would usually be tax deductible.

Source

1 Includes the Medicare Levy.

Click here to download this article in PDF format.

Important information and disclaimer

This publication has been prepared by AustAsia Group, including AustAsia Financial Planning Pty Ltd (AFSL 229454) and AustAsia Finance Brokers Pty Ltd (ACL 385068).

Any advice in this publication is of a general nature only and has not been tailored to your personal circumstances. Accordingly, reliance should not be placed on the information contained in this document as the basis for making any financial investment, insurance or other decision. Please seek personal advice prior to acting on this information.

Information in this publication is accurate as at the date of writing, December 2017. Some of the information has been provided to us by third parties. Whilst it is believed the information is accurate and reliable, the accuracy of that information is not guaranteed in any way.

Opinions constitute our judgement at the time of issue and are subject to change. Neither the Licensee nor any member of AustAsia Group, nor their employees or directors give any warranty of accuracy, nor accept any responsibility, for any errors or omissions in this document.

Any general tax information provided in this publication is intended as a guide only and is based on our general understanding of taxation laws. It is not intended to be a substitute for specialised taxation advice or an assessment of your liabilities, obligations or claim entitlements that arise, or could arise, under taxation law, and we recommend you consult with a registered tax agent.